TWD Monthly Market Update – September 2025

Broader Market Moves¹

Macro Commentary

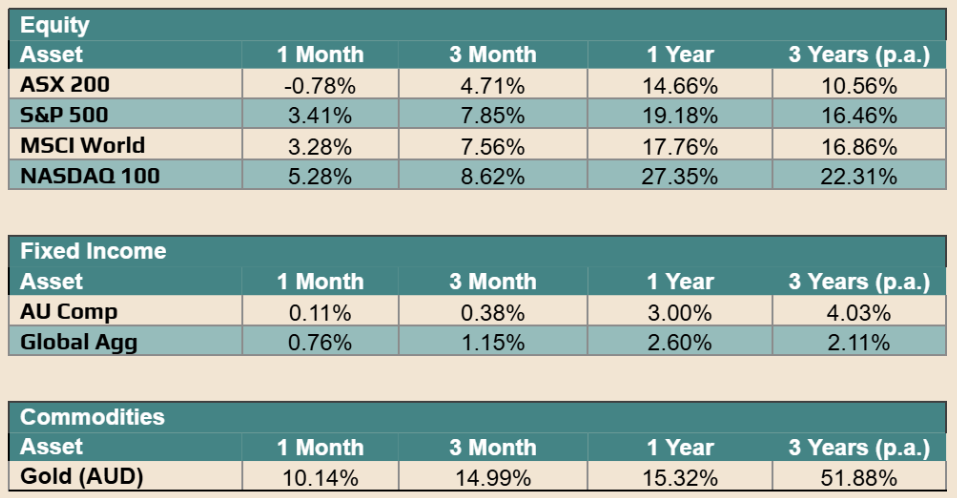

The Australian share market softened over September, breaking a five-month winning streak as investors weighed mixed domestic data, shifting interest rate expectations, and renewed volatility in global bond markets. The S&P/ASX 200 fell around 0.78% over the month to close at 8,848.80. Sector performance was uneven. Materials led gains, supported by stronger prices for copper and gold, while Information Technology also advanced modestly. However, Consumer Staples, Healthcare, Energy, Financials and A-REITs all declined, reflecting continued caution around inflation trends and the outlook for interest rates. Rising bond yields and subdued consumer sentiment further weighed on rate-sensitive and defensive sectors, while mining names outperformed as commodity markets strengthened late in the month.

Australian economic data presented a mixed picture. The August Manufacturing PMI rose to 53.0, its fastest pace of expansion since 2022, pointing to resilience in domestic production and new orders. Q2 GDP grew 0.6%, defying expectations of a contraction, helped by steady household spending despite a decline in the savings rate. However, employment data for August showed a small net loss of jobs, mainly in full-time positions, suggesting some early signs of labour market softening. Inflation ticked higher to 3% in August, driven largely by rising household electricity bills after temporary state rebates expired, tempering expectations for near-term rate cuts by the Reserve Bank. Valuations remained elevated, with the broader market trading well above long-term averages and earnings results generally falling short of expectations.

Global markets were more resilient, supported by optimism that monetary easing in the United States could continue into 2026. The S&P 500 rose about 3.41% over the month as strength in large technology names helped offset softer economic data. The U.S. Federal Reserve cut its policy rate by 25 basis points to a range of 4.00–4.25%, its first reduction since late 2024, citing weaker employment growth and the need to sustain economic momentum. Inflation indicators were mixed: producer prices declined slightly, while core CPI held steady at 3.1% year-on-year. Business surveys showed moderating but still positive activity across manufacturing and services. Investor sentiment remained sensitive to data releases, with markets balancing optimism over policy support against concerns about persistent inflation and stretched valuations in some growth sectors.

In commodities, gold extended its rally through September, climbing to US$3,854.41 an ounce as investors sought safety amid policy uncertainty and geopolitical tension. Oil prices recovered after a soft start, with WTI rising from roughly US$64 to just above US$66 per barrel, supported by supply disruptions and lower U.S. inventories. By September 30, the price declined to USD 63.17, reflecting market adjustments and possibly profit-taking after the mid-month rally.

Looking ahead, markets are likely to remain cautious into the December quarter. Investor focus will remain on inflation trends, central bank policy signals, and the trajectory of global growth. While signs of moderation in inflation and labour conditions may support a gradual policy easing cycle, ongoing geopolitical risks and high valuations could limit upside momentum. Domestically, further weakness in consumption or employment could prompt the RBA to adopt a more accommodative stance, while stabilising commodity demand from key trading partners would be supportive for local resource stocks. Overall, volatility may stay elevated, but selective opportunities remain across quality cyclical and resource exposures as the global economy adjusts to a slower but more balanced growth environment.

DISCLAIMER:

The contents of this publication are only intended to provide a summary and general overview of matters of interest in the financial markets and in the economy and are distributed in order to promote broad discussion. The publication does not constitute investment or financial product advice, it does not constitute an offer or invitation to purchase a financial product or financial service, nor does it of itself create a client-financial adviser relationship. To the extent that any part of the contents of this publication may be said to constitute “general advice” we warn you not to act on any matter referred to in this publication without first seeking qualified financial product advice appropriate to your particular circumstances, needs and objectives before acting or relying on any content in this publication. TWD Licensee Services Pty Ltd (ABN 88 605 064 480 – AFSL 475964) makes no warranties or representations about the accuracy or completeness of the content of this publication, and excludes, to the maximum extent permissible by law, any liability which may arise as a result of the use of the content of this publication.