TWD Monthly Market Update – August 2025

Broader Market Moves1

Macro Commentary

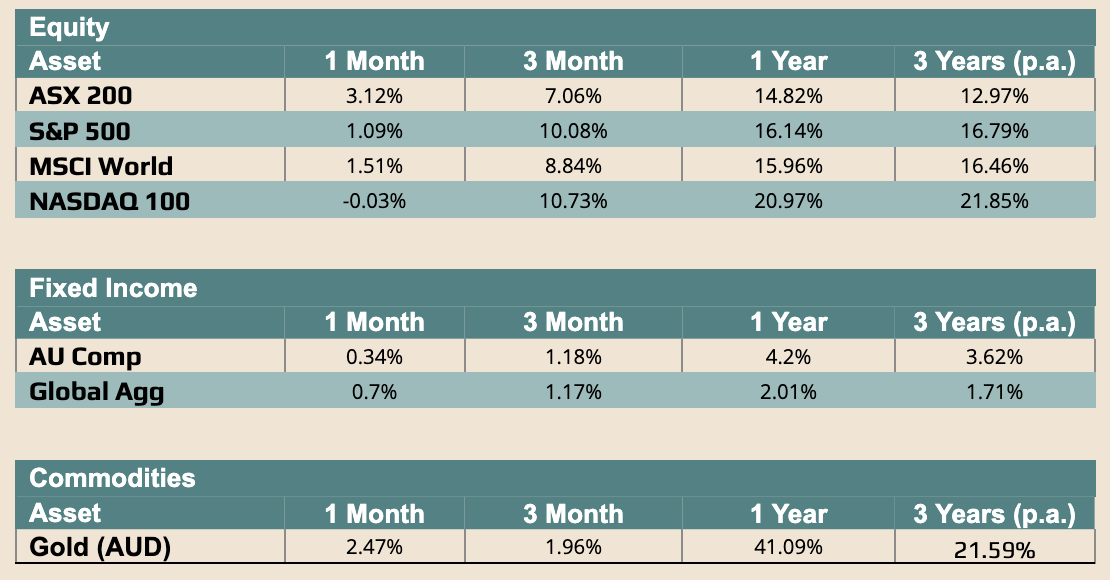

August saw modest gains in Australian equity markets, with the ASX 200 rising approximately 3.12%, supported notably by strong resource and financial sector performance. Globally, markets performed more robustly. The S&P 500, along with key European and Japanese indices, delivered solid returns amidst growing optimism that inflation pressures were easing and central banks may be approaching the end of their rate-hiking cycles.

In Australia, the Reserve Bank of Australia (RBA) reduced the official cash rate by 25 basis points to 3.60% on 12 August, marking the third cut of the year. The move was widely anticipated and accompanied by a revision to its medium-term labour productivity forecast, now trimmed from 1.0% to 0.7% per annum. This downgrade underscores structural challenges like weak business investment and regulatory burdens, which collectively are expected to weigh on potential economic growth.

Labour market data for July reinforced the narrative of resilience. Employment rose by approximately 24,500 in seasonally adjusted terms, while full-time employment jumped by 60,500 and part-time roles declined by 35,900. The unemployment rate eased from 4.3% to 4.2%, and female full-time employment surged by around 40,000, contributing to a record high in female labour force participation.

The underlying strength in employment has tempered expectations for an RBA cut in September, shifting market focus instead to November as the likely timing for the next move. Australia’s Composite PMI continued to signal expansion, though reporting season painted a mixed picture: firms missing earnings were heavily penalised, while positive surprises were met with more muted investor reactions.

Across the Pacific, the U.S. stock market held up well through August, with gains anchored by the technology and consumer discretionary sectors. Investors kept one eye on softening employment data and another on encouraging growth metrics. Initial jobless claims rose modestly mid-month, pointing to some labour market softness, though private-sector surveys indicated ongoing staffing gains. In activity data, Q2 GDP rebounded to a strong 3.3% annualised growth, driven by consumer spending, business investment, and an unexpected hit to imports. Core PCE inflation, the Federal Reserve’s preferred gauge, ticked up slightly, reinforcing expectations that the Fed may start reducing rates as soon as September.

At Jackson Hole, Fed Chair Jerome Powell spoke to this backdrop of sticky but moderating inflation, indicating the Fed’s readiness to pivot should the labour market soften further.

Trade developments added to the backdrop of uncertainty. The U.S.–China tariff truce was extended for another 90 days, delaying planned hikes, though existing tariffs remain in place. In a separate development, the U.S. introduced 50% tariffs on a broad set of Indian exports in response to New Delhi’s continued discounted oil purchases from Russia.

Commodity markets reflected a cautious mood with gold prices edging higher, bolstered by safe-haven demand and geopolitical uncertainty, though strong U.S. data capped upside. Oil prices increased, supported by supply constraints, steady demand, and elevated trade tensions.

Looking forward, inflation trends in both Australia and the U.S. will be pivotal in shaping central bank actions through the end of the year. In Australia, markets now see a final rate cut likely in November, conditional on sustained easing of price pressures. In the U.S., the Fed appears increasingly positioned to begin rate reductions as early as September, depending on upcoming data.

DISCLAIMER:

The contents of this publication are only intended to provide a summary and general overview of matters of interest in the financial markets and in the economy and are distributed in order to promote broad discussion. The publication does not constitute investment or financial product advice, it does not constitute an offer or invitation to purchase a financial product or financial service, nor does it of itself create a client-financial adviser relationship. To the extent that any part of the contents of this publication may be said to constitute “general advice” we warn you not to act on any matter referred to in this publication without first seeking qualified financial product advice appropriate to your particular circumstances, needs and objectives before acting or relying on any content in this publication. TWD Licensee Services Pty Ltd (ABN 88 605 064 480 – AFSL 475964) makes no warranties or representations about the accuracy or completeness of the content of this publication, and excludes, to the maximum extent permissible by law, any liability which may arise as a result of the use of the content of this publication.