TWD Monthly Market Update – March 2026

Broader Market Moves1

Macro Commentary

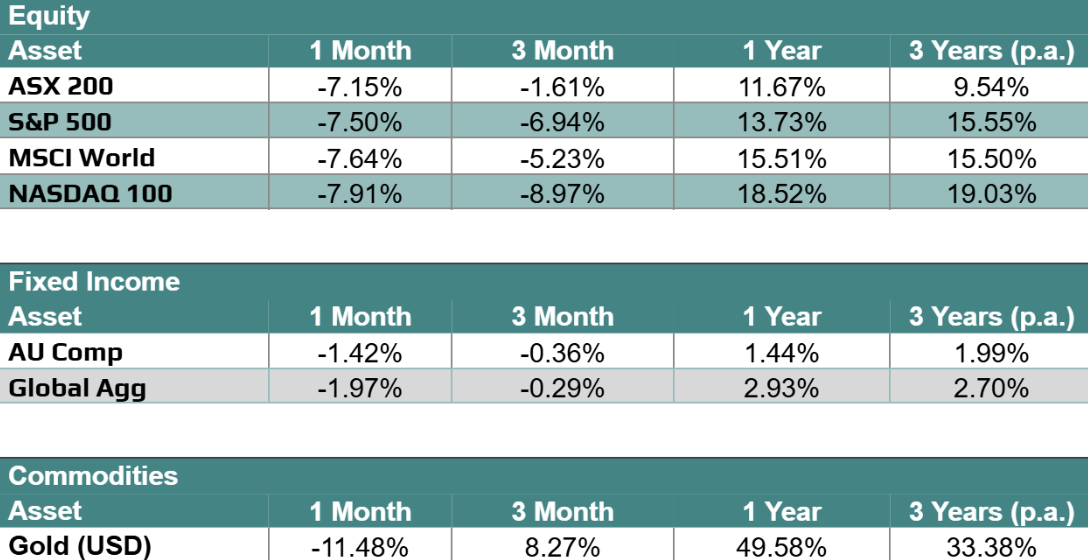

The Australian equity market weakened through March, reflecting a shift in investor sentiment as rising energy prices and escalating geopolitical tensions increasingly dominated market dynamics. The S&P/ASX 200 declined by approximately 7% over the month. Sector performance diverged meaningfully. Energy stocks outperformed on the back of sharply higher oil prices, while financials provided some relative stability. In contrast, growth-oriented sectors including technology and healthcare lagged as higher interest rate expectations weighed on valuations. Materials were more volatile, reflecting ongoing uncertainty around China’s growth outlook and commodity demand.

Domestic economic conditions remained broadly resilient, though increasingly secondary to global developments. The Reserve Bank of Australia raised the cash rate by 25 basis points to 4.10%, reinforcing its focus on persistent inflation pressures. Labour market data for February showed continued strength, with employment increasing and participation rising to 66.9%, while the unemployment rate edged higher to 4.3% as labour supply expanded. Business activity softened through the month, with PMI data indicating moderating conditions and pointing to a mild contraction in private sector activity by quarter-end. Importantly, most data released through March reflects February conditions and is unlikely to fully capture the impact of escalating Middle East tensions and higher energy prices. Upcoming releases will provide a clearer indication of how these developments are feeding through to inflation, activity and confidence. Overall, the economy remains on a solid footing, albeit with signs of gradual slowing as higher interest rates take effect.

Global equity markets followed a similar pattern, though with more pronounced weakness. The S&P 500 declined by approximately 5.0% on a total return basis over the month, as markets reassessed the outlook for inflation and interest rates. Sector performance reflected the evolving macro backdrop, with energy outperforming and growth sectors under pressure. Financials remained relatively resilient, while defensive sectors saw modest inflows. The move represented a pullback from recent highs, as markets contended with higher energy costs and a prolonged restrictive policy environment.

US economic data continued to point to moderating but still positive growth. Indicators of first quarter activity remained consistent with expansion, supported by resilient consumption, though momentum has eased from earlier in the cycle. Inflation remained relatively contained on a backward-looking basis, with headline CPI at 2.4% year-on-year and core CPI at 2.5%, though underlying price pressures continue to limit the Federal Reserve’s flexibility. Labour market data indicated some cooling, with softer payroll outcomes and a modest rise in unemployment, though conditions remain far from weak. As with Australia, much of the data released through March reflects February conditions and does not yet fully capture the impact of recent geopolitical developments and rising energy prices. Upcoming data will be key in assessing how these factors feed through to inflation and activity. The Federal Reserve maintained its policy rate at its March meeting, reiterating a data-dependent approach and signalling that further progress on inflation is required before easing can be considered.

Commodity markets were the defining feature of March, increasingly driving rather than reflecting broader market movements. Oil prices rose sharply and remained elevated at month-end, reflecting a significant geopolitical risk premium and heightened concern around potential disruptions to Middle East supply routes. This has fed directly into inflation expectations and has been a key driver of equity market weakness. Gold prices, while volatile, were lower overall across the month. After declining through early March, prices recovered into month-end as safe-haven demand re-emerged alongside escalating geopolitical risks, though this rebound was insufficient to offset earlier weakness.

Looking forward, the market narrative has shifted, with energy and geopolitics now the primary drivers of global macro conditions. The key transmission mechanism remains oil, with higher prices feeding into inflation expectations and complicating the path for central banks. While policymakers appear reluctant to tighten policy further, energy-driven inflation may delay the timing of any easing cycle.

Our base case is that oil prices do not follow a simple path lower from here. While prices may ease from peak levels, they are unlikely to return quickly to pre-conflict norms. Instead, a sustained geopolitical premium is likely to persist, creating a higher floor for energy prices while leaving the upside sensitive to how the conflict evolves. The most probable outcome is not one of extreme disruption, but of ongoing friction, where partial and uncertain supply conditions keep markets supported without triggering a full-scale supply shock.

The key variable remains duration. A short-lived disruption can be absorbed by markets and supply chains, but a more prolonged period of elevated prices would increasingly feed into the real economy through weaker consumption, margin pressure and softer confidence. In this environment, growth is likely to slow but not break, while inflation remains elevated in the near term and policy flexibility remains constrained.

From a portfolio perspective, the current environment reinforces the importance of diversification across asset classes and regions. While higher energy prices support commodity-linked exposures in the near term, they also introduce broader risks to growth and policy stability. Balancing these competing forces remains central to navigating the evolving macro landscape.

1ASX 200 refers to SPDR S&P ASX 200 Fund (STW), S&P 500 refers to iShares S&P 500 (AUD Hedged) ETF, MSCI World refers to Vanguard MSCI Index International Shares (Hedged) ETF, NASDAQ 100 refers Nasdaq 100 Currency Hedged ETF, AU Comp refers to the Vanguard Australian Fixed Interest Index ETF, Global Agg refers to Vanguard Global Aggregate Bond Index (Hedged) ETF, Gold (USD) refers to the LSEG Gold Spot Price (USD)

DISCLAIMER:

The contents of this publication are only intended to provide a summary and general overview of matters of interest in the financial markets and in the economy and are distributed in order to promote broad discussion. The publication does not constitute investment or financial product advice, it does not constitute an offer or invitation to purchase a financial product or financial service, nor does it of itself create a client-financial adviser relationship. To the extent that any part of the contents of this publication may be said to constitute “general advice” we warn you not to act on any matter referred to in this publication without first seeking qualified financial product advice appropriate to your particular circumstances, needs and objectives before acting or relying on any content in this publication. TWD Licensee Services Pty Ltd (ABN 88 605 064 480 – AFSL 475964) makes no warranties or representations about the accuracy or completeness of the content of this publication, and excludes, to the maximum extent permissible by law, any liability which may arise as a result of the use of the content of this publication.