TWD Monthly Market Update – October 2025

Broader Market Moves¹

Macro Commentary

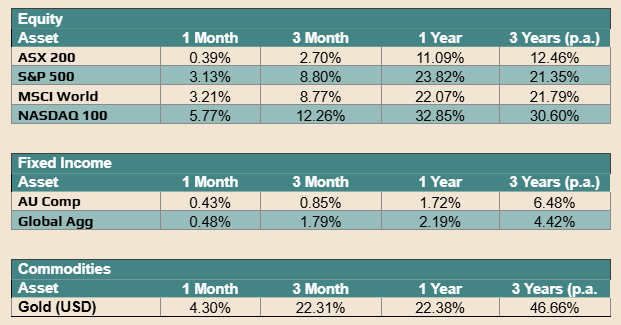

The Australian share market saw heightened volatility in October but ultimately ended the month roughly flat. After a strong start that briefly pushed the S&P/ASX 200 to a record intraday high above 9,100, the index gave back gains and closed +0.39% on a total return basis. Sector performance was mixed. Resource and commodity-linked names provided bright spots as gold miners rallied on record bullion prices, and Energy was relatively resilient as oil prices firmed. In contrast, rate-sensitive and consumer-facing areas lagged. Consumer Discretionary sold off following the hot inflation print, while A-REITs struggled as bond yields rose and the rate outlook turned more pessimistic. Healthcare also underperformed late in the month after stock specific weakness, with CSL’s guidance cut prompting a sharp single-day decline. Breadth was uneven as investors weighed persistent inflation against a softer growth pulse and higher yields.

Australian macro data delivered a mixed message that ultimately pushed rate cut hopes further out. The labour market softened, with the September unemployment rate lifting to 4.5 percent despite a modest rise in jobs. That initially nudged market pricing toward a near-term RBA cut as a growth cushion. The narrative flipped with Q3 CPI, which rose 1.3 percent quarter on quarter and lifted annual inflation to 3.2 percent from 2.1 percent in Q2. Trimmed mean core inflation rose 1.0 percent, above expectations, and reinforced that price pressures remain above the 2 to 3 percent target band. Power prices, as earlier rebates rolled off, and holiday travel costs were notable contributors. Markets quickly marked down the probability of a November move and now expect the cash rate to remain on hold well into 2026 unless activity slows materially.

Global equities advanced modestly. In the United States, the S&P 500 rose +2.34% in October on a total return basis in USD, marking another monthly gain and setting fresh mid-month highs. The leadership remained narrow. Several of the Magnificent Seven delivered strong Q3 results that lifted sentiment, including robust cloud and digital advertising updates from the mega caps. These companies now comprise a very large share of index market cap, which helped mask more subdued gains across the broader index. So far, earnings season has been strong, with a high beat rate and guidance that was steady rather than exuberant, which was enough to sustain risk appetite.

The MSCI World ex Australia index also posted a modest gain in local currency terms. Japan contributed positively on improved earnings revisions and corporate reform momentum, while parts of Europe and several emerging markets lagged on softer activity data and lingering geopolitical risk. With the government currently shut down, US macroeconomic data has been less frequent than usual, with jobs data releases cancelled. Headline CPI, released towards the end of the month grew by 3.0% year on year in September, indicating that disinflation has slowed but not reversed. Towards the end of the month, the Federal Reserve reduced the Fed Funds rate by 0.25% at its late October meeting to a 3.75%-4.00% percent range and reiterated data dependence. Chair Powell’s tone was cautious on the prospect of further near-term cuts, citing the need for clearer evidence that inflation is returning to target.

Commodities were mixed and volatile. Gold spiked to fresh records, then retraced, and finished the month around US$4,013 per ounce, which implies roughly a one month return of +4.30% percent and a one year gain near +50% in USD terms. Elevated retail demand for physical bars and coins was evident early in the month, followed by some positioning unwind as prices swung. Oil drifted lower into month end, with WTI around US$60.57 per barrel. Softer demand signals and steady non-OPEC supply kept prices range bound, which if sustained would modestly ease headline inflation pressures in Australia.

Looking ahead, we expect a cautious tone to persist through November and into the December quarter. Investor attention will stay on the path of inflation, central bank messaging, and the durability of global growth. Signs of gradual disinflation and softer labour conditions could support a measured easing cycle in 2026, but valuations remain full and geopolitical risks are still present, which may cap near-term upside. In Australia, any further weakness in consumption or employment would increase the likelihood of a more supportive RBA stance. Into year-end, we anticipate pockets of volatility as liquidity thins and earnings revisions settle. Selectivity remains important, with a preference for quality cyclicals tied to infrastructure and commodity supply, resource producers with strong balance sheets, and companies demonstrating pricing power. Defensive duration in fixed income can help balance equity risk.

DISCLAIMER:

The contents of this publication are only intended to provide a summary and general overview of matters of interest in the financial markets and in the economy and are distributed in order to promote broad discussion. The publication does not constitute investment or financial product advice, it does not constitute an offer or invitation to purchase a financial product or financial service, nor does it of itself create a client-financial adviser relationship. To the extent that any part of the contents of this publication may be said to constitute “general advice” we warn you not to act on any matter referred to in this publication without first seeking qualified financial product advice appropriate to your particular circumstances, needs and objectives before acting or relying on any content in this publication. TWD Licensee Services Pty Ltd (ABN 88 605 064 480 – AFSL 475964) makes no warranties or representations about the accuracy or completeness of the content of this publication, and excludes, to the maximum extent permissible by law, any liability which may arise as a result of the use of the content of this publication.

¹ ASX 200 refers to SPDR S&P ASX 200 Fund (STW), S&P 500 refers to iShares S&P 500 (AUD Hedged) ETF, MSCI World refers to Vanguard MSCI Index International Shares (Hedged) ETF, NASDAQ 100 refers Nasdaq 100 Currency Hedged ETF, AU Comp refers to the Vanguard Australian Fixed Interest Index ETF, Global Agg refers to Vanguard Global Aggregate Bond Index (Hedged) ETF, Gold (USD) refers to the LSEG Gold Spot Price (USD)